Digital Health After the Shutdown: Relief, Resets, and Unresolved Risk

The Firewire is an opportunity to step back from the daily noise and look at what actually moved the healthcare and digital health landscape over the past few weeks—and why it matters.

This month’s signals span policy, capital, and technology: a government shutdown that ended without resolving structural uncertainty; CMS nudging the market more forcefully toward value-based care; consolidation and funding flows favoring scale and payer alignment; and steady advances in AI and interoperability that promise progress, even if not overnight transformation.

Relief after government shutdown, long-term consequences loom

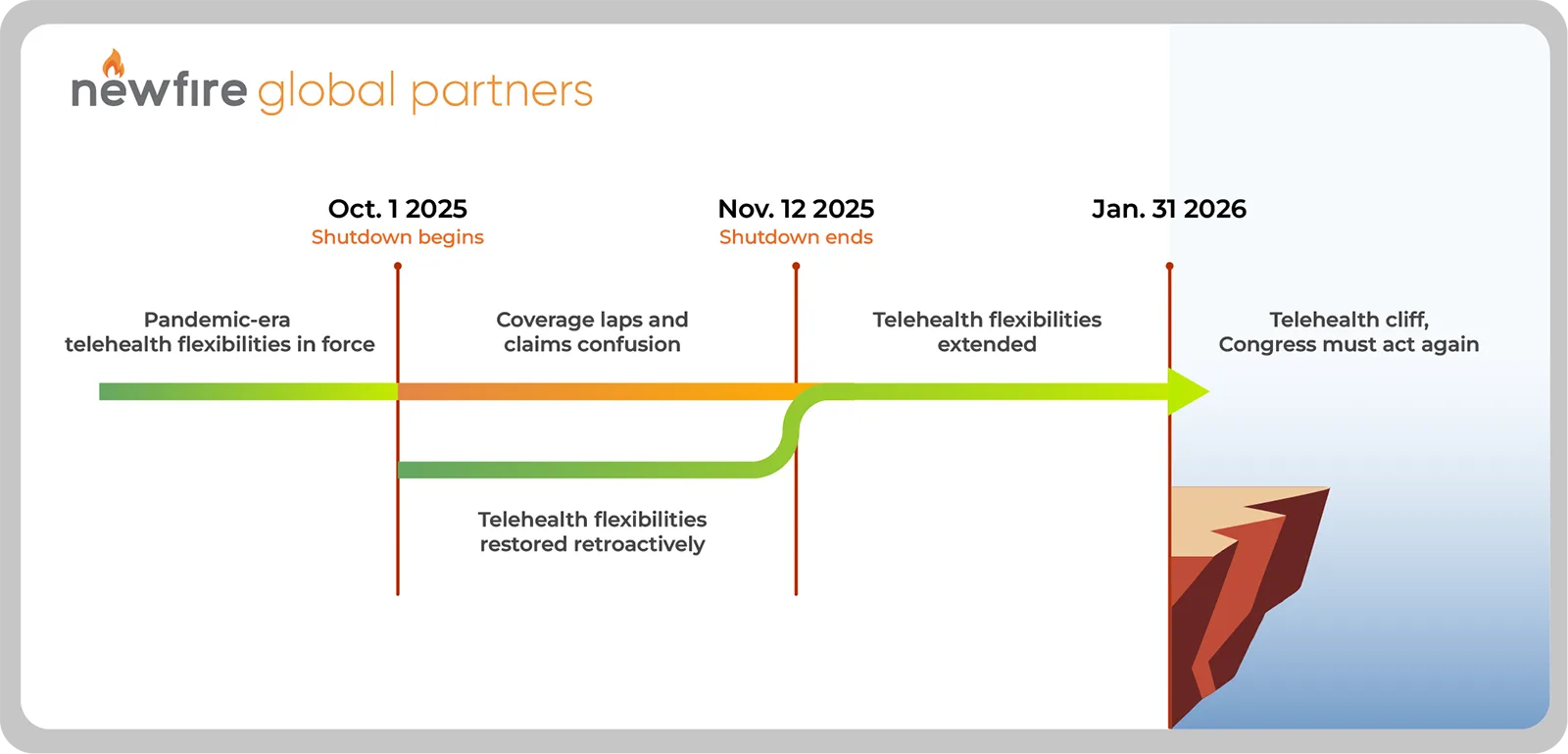

The federal government resumed operations on November 12, and although the historic shutdown lasted 43 days, its effects are likely to be felt well into 2026 and beyond. With delays to FDA approvals, NIH grant holds, and ONC’s interoperability efforts, digital health operators can expect a backlog of regulatory updates in Q1 2026. Here’s what else is new in policy and regulation as we end this year.

Medicare telehealth flexibilities restored through January 30, 2026

Digital health companies breathed a sigh of relief with the shutdown ending, and none more so than telehealth operators serving Medicare FFS populations. For them, Congress passing a Continuing Resolution (CR) that ended the shutdown means that Medicare FFS telehealth flexibilities that had lapsed on October 1 are now restored retroactively and extended through January 30, 2026.

This is, of course, welcome news, but what concerns me is the short period that signals we’re heading for another “telehealth cliff” in just a few months. For a government that claims to be “taking steps to expedite the adoption and awareness of telehealth,” it remains stubbornly hesitant to provide an environment where this model can thrive.

While FFS telehealth services continue to have an uncertain future until these reimbursement models are made permanent, the ACCESS program CMS announced this month – to much fanfare from the digital health community, see below – is where this administration appears to be placing its bets for digital health.

Health Insurance Privacy Reform Act introduced

On the consumer technology front, Louisiana Senator Bill Cassidy introduced new legislation aimed at closing a long-felt gap and extend HIPAA-style protections to health information collected by health apps, wearables, and wellness platforms. The Health Information Privacy Reform Act (HIPRA) would bring HIPAA‑like obligations to health apps, wearables, and wellness platforms, but it leaves many details—such as how far protections reach into inferences, recommendations, and AI‑generated insights—to future HHS rulemaking.

Here at Newfire, we’ve been proponents of such regulations for some time. In fact, two of our recent podcast episodes on patient data access, with Deven McGraw, a leading voice in healthcare regulation and Paul Wilder, Executive Director of CommonWell Health Alliance, have called for it directly.

CMS launches ACCESS Model, expanding value-based care across four clinical domains

CMS has announced a new innovation model, ACCESS (Advancing Chronic Care with Effective Scalable Solutions), targeting “conditions affecting 2/3rds of the Medicare population” – specifically diabetes, maternal health, behavioral health, and musculoskeletal care. The program introduces domain-specific attribution, PMPM fees, and shared-savings mechanics, creating clearer pathways for digital health companies to participate in outcomes-based reimbursement while servicing traditional Medicare (which in itself is an interesting development). Behavioral health represents the largest immediate opportunity given the general acceptance of teletherapy, while maternal health offers particularly attractive margins through episode-based payments.

ACCESS stands out for its specificity. By defining domains, attribution rules, and payment mechanics upfront, CMS is signaling exactly where it wants innovation to land. For healthtech companies, this shifts the question from whether to engage with value-based care to whether they’re operationally ready to take real clinical and financial risk.

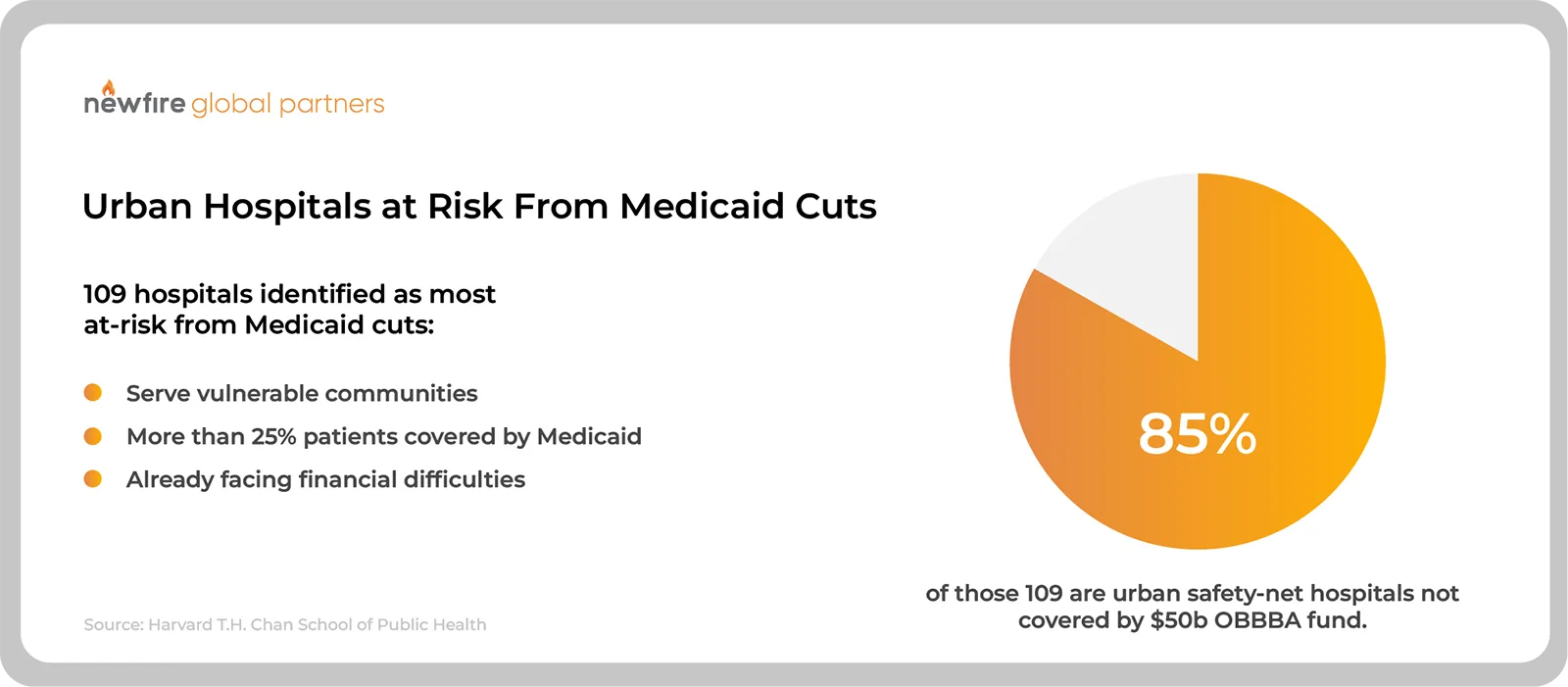

Urban safety-net hospitals face greatest risk from medicaid cuts

Bringing our policy and regulation analysis full circle, a Harvard study found that it is urban safety-net hospitals that may be most adversely impacted by OBBBA Medicaid cuts — a key point of contention in negotiations that led to the shutdown.

Why is this alarming? Previous analyses warned that Medicaid cuts would endanger rural hospitals that serve vulnerable communities, caring for large Medicare populations, and already experiencing financial difficulty. Which is why policymakers included a $50 billion provision to bolster rural hospitals. Now, however, this new Harvard analysis shows that a vast majority of the most at-risk hospitals are actually in urban areas and therefore ineligible for that support. There’s no question there’s a crisis in rural health today, and now it sounds like that crisis is going to shift into more urban settings in the years ahead.

This is just one example of how broad-stroke OBBBA cuts can have unexpected consequences on sprawling systems such as healthcare, where real lives are at stake. Unfortunately, it probably won’t be the last.

Funding and M&A signal a shift toward scale and payer alignment

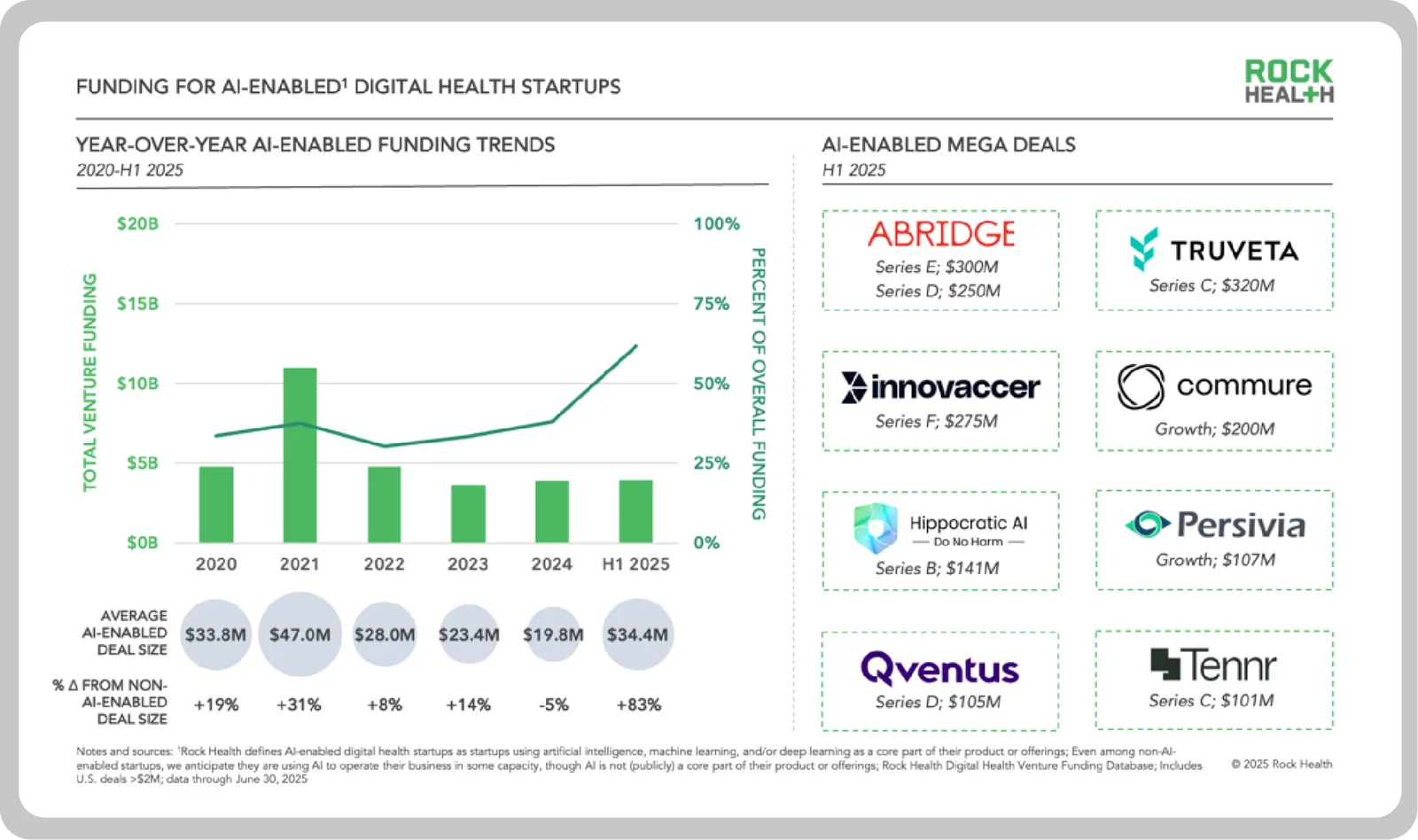

Despite a challenging funding environment, capital is still flowing to healthcare companies with clear scale advantages, strong data assets, and credible AI strategies. According to PitchBook, Q3-2025-PitchBook-NVCA-Venture-Monitor.pdfventure capital funding for healthcare technology startups through Q3 has already surpassed 2024’s full-year total, with $3.9 billion raised in Q3 alone. Rock Health’s mid-year report further underscores the trend: AI-enabled startups captured 62% of digital health venture funding in the first half of 2025, commanding significantly larger rounds than their non-AI peers.

That same pattern is playing out at the enterprise level, where consolidation and platform expansion are defining the year’s most consequential deals.

GE HealthCare Acquires Intelerad for $2.3 Billion

GE HealthCare announced it would acquire Montreal-based cloud imaging software provider Intelerad for $2.3 billion in cash. The acquisition is being viewed as proof GEHC is serious about transforming from a hardware manufacturer to a vertically integrated solution provider—one that is “digital, intelligent and cloud-native.”

Intelerad was a key independent player in enterprise imaging (PACS/RIS). To me, this acquisition signals the end of the “best-of-breed” era in imaging IT, pushing hospital CIOs toward consolidated “glass-less” enterprise platforms.

Abbott acquires Exact Sciences for $21 billion

In the largest deal of the year for our sector (that I’m aware of), Abbott signed a definitive agreement to acquire Exact Sciences. According to a press release, “Abbott will acquire all outstanding shares of Exact Sciences for $105 per common share in cash, at a total equity value of approximately $21 billion and an estimated enterprise value of $23 billion.” This equates to an approximate 50% premium, which should make shareholders happy.

The reasoning behind the massive payout is clear: this is a diagnostics deal, with an immensely powerful data dividend. Exact Sciences’ massive screening infrastructure (Cologuard) gives Abbott direct-to-patient access and a foothold in home-based screening, expanding on the traditional lab-centric model. They’ll also gain a new channel to access candidates for clinical trial recruitment and a resource for real-world outcomes monitoring. Obviously this still needs to be approved by regulators, but I can’t foresee any roadblocks that would stop it from going through.

DUOS raises $130M growth equity

In a dry funding landscape, the care navigation platform, DUOS, secured $130 million “to scale its AI benefits platform for seniors.” The funding is to be used to scale DUOS’ AI capabilities while, and this is the interesting part, getting it market ready for Medicare Advantage, Medicaid and ACA marketplace plans nationwide.

DUOS is showing the healthtech startup scene that there’s an easy route to funding in the current landscape: instead of just offering run-of-the-mill provider software, find ways to solve payer problems like member engagement and benefits navigation.

Tech & innovation news promises future unburdening and simplification for healthcare sector

Technology and innovation news this month underscores a broader shift in healthcare: progress is coming not from a single breakthrough, but from the steady reinforcement of core infrastructure and tools. Interoperability frameworks are maturing, large platforms are repositioning around AI and data exchange, and frontier models are beginning to move beyond narrow assistance toward task-level autonomy. Together, these developments point to a healthcare ecosystem that is incrementally better equipped to reduce friction—both clinical and administrative—even as questions remain about where real, durable value will ultimately emerge.

Oracle Health designated as QHIN under TEFCA

November also marked an important milestone for healthcare interoperability. Oracle Health Information Network was designated as a Qualified Health Information Network under TEFCA, the 11th data exchange to receive QHIN status. For those keeping count, that’s more than double the number when TEFCA went live in late 2023.

Oracle is heralding this as an advancement in “harnessing the power of AI, improving quality of care and health outcomes, and scaling value-based care,” but are the long-term implications really that significant? Newfire’s own Interoperability Lead weighs in:

This is an expected move for a vendor of Oracle’s size. After years of underinvestment, they’re rebuilding their platform to stay competitive—but this feels more like a "must-do" move than a breakthrough. Epic is far ahead in driving real customer value from interoperability networks, and many in the industry remain skeptical about how much new value QHINs will add beyond existing networks. That said, Epic’s strong push behind TEFCA is a promising signal for the broader future of QHINs.

Brendan Iglehart, Interoperability Practice Lead

Frontier AI models move closer to more robust task‑level reasoning

We’ve seen a flurry of LLM releases lately headed in the same direction: agentic autonomy, reduced hallucinations, and encroaching reasoning capabilities.

At Ignite 2025, Microsoft pitched a Copilot that is fast becoming a first-class coworker instead of a mere smart assistant with a suite of AI agents that are designed to integrate more seamlessly with its flagship AI platform. Anthropic is even going a step further. The new Claude Opus 4.5 was benchmarked against Anthropics own performance engineering candidates in an exam designed to assess technical ability and judgement under time pressure. According to Anthropic, the new model “scored higher than any human candidate ever,” raising more questions about the future of the software engineering profession.

For digital health providers, the rising accuracy and autonomy of AI tools points to a future in which they will have an opportunity to alleviate some of the most acute symptoms of today’s overwhelmed healthcare system, from prior authorization routing and claims adjudication to clinical triage.

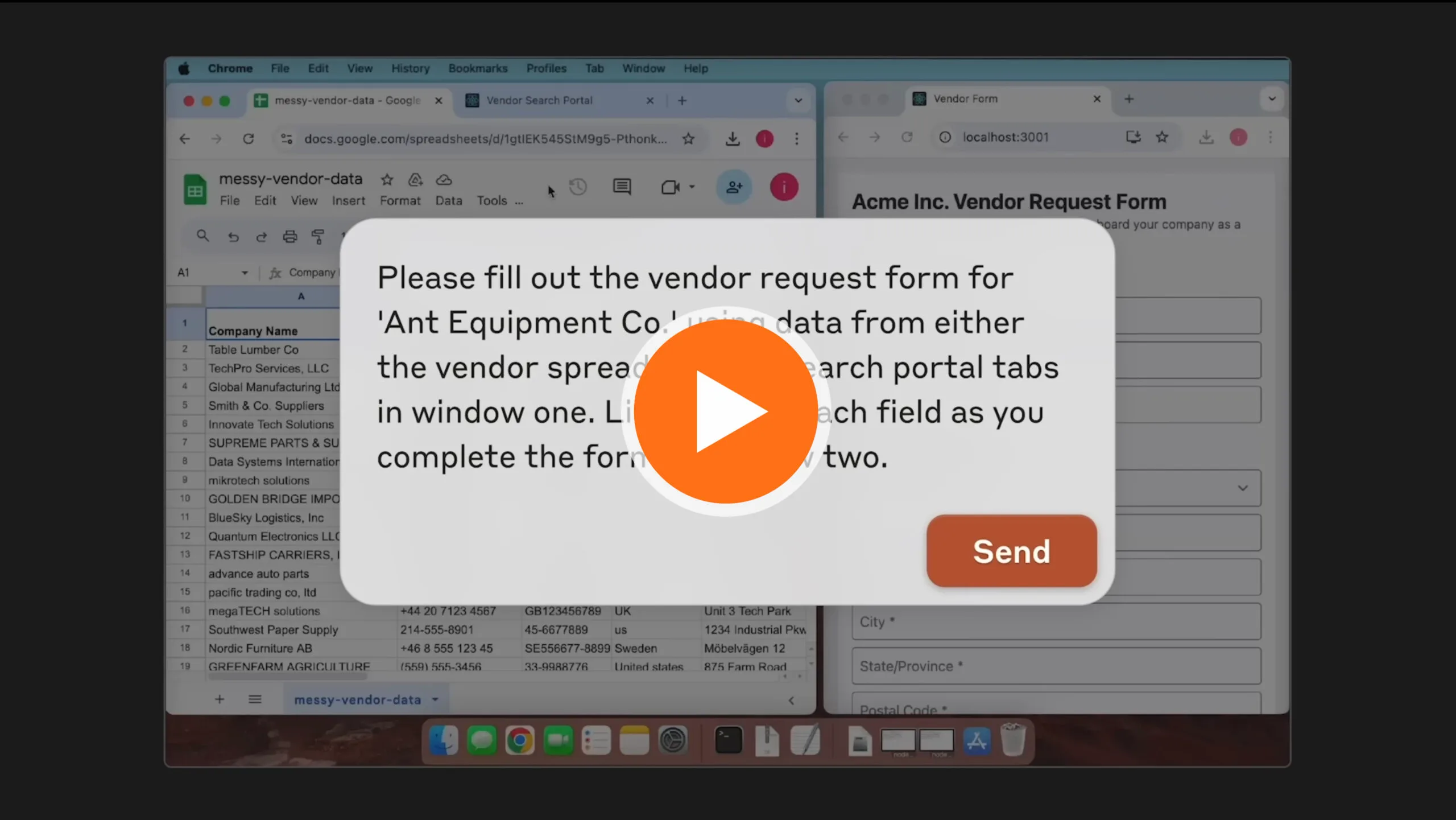

“Computer use” breaks down the GUI barrier

Amidst the agentic AI hype, there was another announcement from Anthropic you may have missed, but has equal bearing on the effort to unburden healthcare administration: the introduction of the computer use capability. In essence, this feature allows developers to direct Claude to use computers as a human would: moving cursors, pushing buttons, and writing text.

Computer use is now in public beta for Claude 3.5 Sonnet, meaning there are still many kinks to iron out. But the potential here is massive: down the line, we can easily imagine automation of tasks such as looking up coverage, filling out forms across the care cycle, and querying legacy EHRs without APIs.

With digital health back in business, what’s next for you?

With the government back online, digital health has regained its footing—but the past few months made one thing clear: momentum alone isn’t enough. Policy uncertainty, funding pressure, and infrastructure gaps continue to separate companies built for scale from those built for headlines. The next phase will favor teams that can navigate regulation, align with payer incentives, and translate technology into measurable outcomes.

If you’re wrestling with these shifts—whether around interoperability, value-based care, AI adoption, or go-to-market strategy—we’d welcome the conversation. At Newfire, we work alongside operators and executives to turn complexity into forward motion. Let’s compare notes and explore what comes next.