Inside HLTH 2025, Market Realignment, and the Next Phase of Healthcare AI

Welcome to the first edition of “The Firewire.” Each month, I’ll share my perspectives on what I believe are some of the most important developments in healthcare and digital health, with a focus on what matters for operators, executives, and investors.

As a Principal within Newfire Advisory, I spend a lot of time looking at where the industry is headed and identifying signals of lasting change (signal) versus short-term hype (noise). My goal here is to share the notable stories from the past month that hold strategic implications for operators in the digital health sector, my editorial notes on the implications, and what to watch for next.

In this issue: key insights from Menlo Ventures, Rock Health, and SVB that reveal how capital, competition, and consolidation are reshaping the healthtech landscape; notable highlights and reflections from HLTH 2025 in Las Vegas; a look at the latest funding and M&A activity pointing to a reopening IPO window; and some interesting takes from industry media over the last month.

What We’re Reading: 2025Q3 Investment Market Reports Galore

Three influential healthtech reports — by Menlo Ventures, Rock Health, and Silicon Valley Bank — converge on a shared message: healthcare’s AI transformation is real, but it’s evolving into a more complex, uneven, and operationally driven market. Across all three, we see the same pattern emerging: record investment paired with concentration, consolidation, and caution.

AI adoption is accelerating fastest in provider operations, yet funding is increasingly controlled by a small circle of mega-investors, valuations are racing ahead of fundamentals, and mid-stage startups are squeezed between hype and proof. What was once innovation for its own sake is now a contest of execution, ROI, and scale.

Menlo Ventures — State of AI in Healthcare 2025

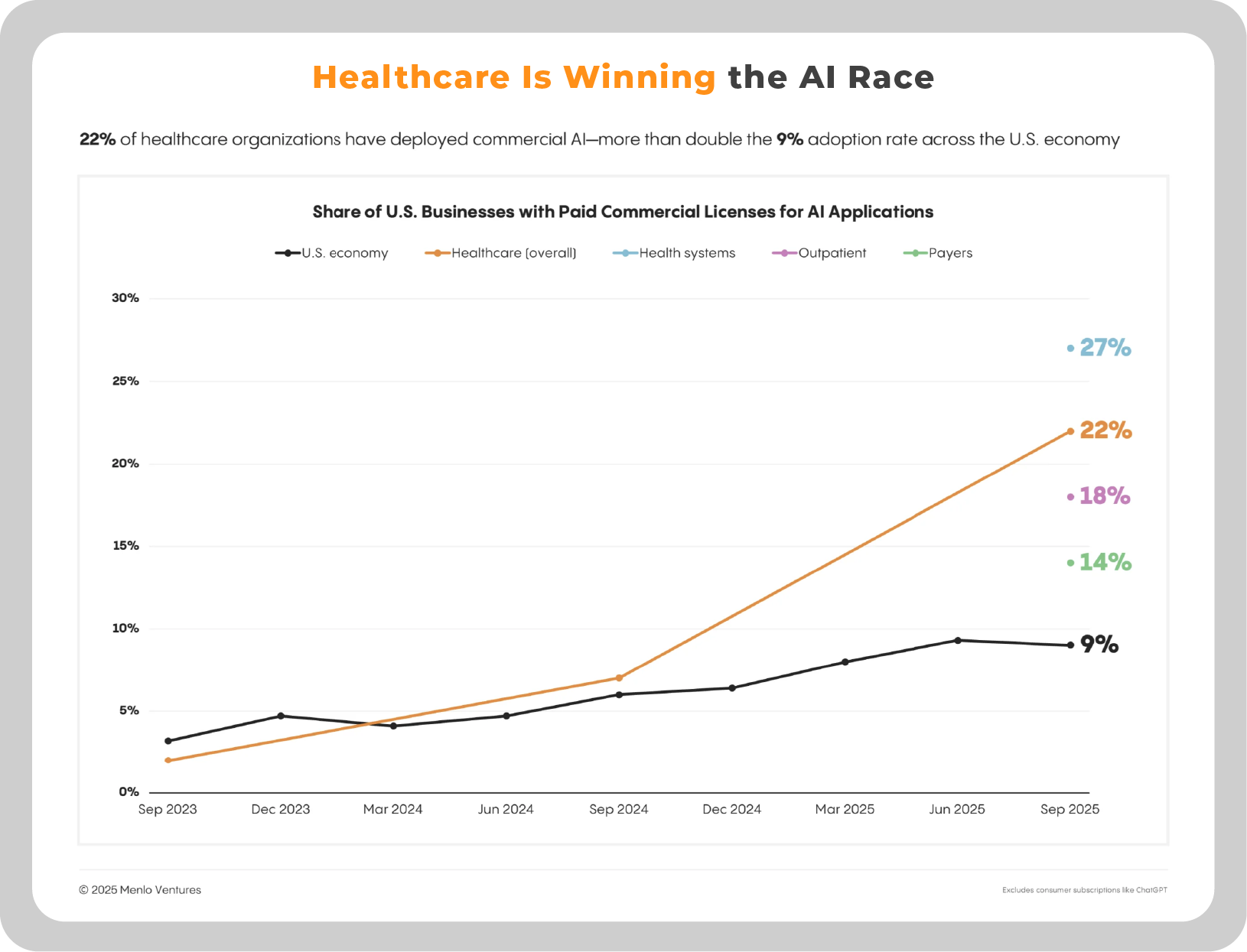

Menlo’s most comprehensive healthcare-AI report yet confirms that transformation is real, but warns of early signs of saturation. Based on surveys of 700+ executives, the report shows that healthcare has become the leading enterprise adopter of AI, with 22% adoption (2.2× faster than other industries) and $1.4 B in spend. Yet, beneath the boom, commoditization and incumbent pressure are already reshaping the field.

Key Findings:

- Healthcare leads enterprise AI adoption: 22% vs. 9% economy-wide; adoption up 7× YoY.

- Startups dominate — for now: 85% of generative-AI spend flows to startups; incumbents are closing fast.

- Ambient scribing is commoditizing: Switching intent is high (67%), signaling an end to easy growth.

- Procurement cycles compressing: Provider buying times down 18-22%; payer cycles slowing.

- “Services-to-software” gap: $740 B in admin costs, only 8.5% digitized—a $677 B automation opportunity.

- Provider-payer AI arms race: Automation may trigger cost and claim surges unless systems align.

- Investor takeaway: Real adoption, but valuations and market concentration pose risks; winners will expand horizontally before commoditization hits.

Bottom Line: Healthcare is no longer a technology laggard. It’s leading AI adoption. But in Menlo’s data, you can already see the next challenge: maturity brings competition, consolidation, and thinner margins.

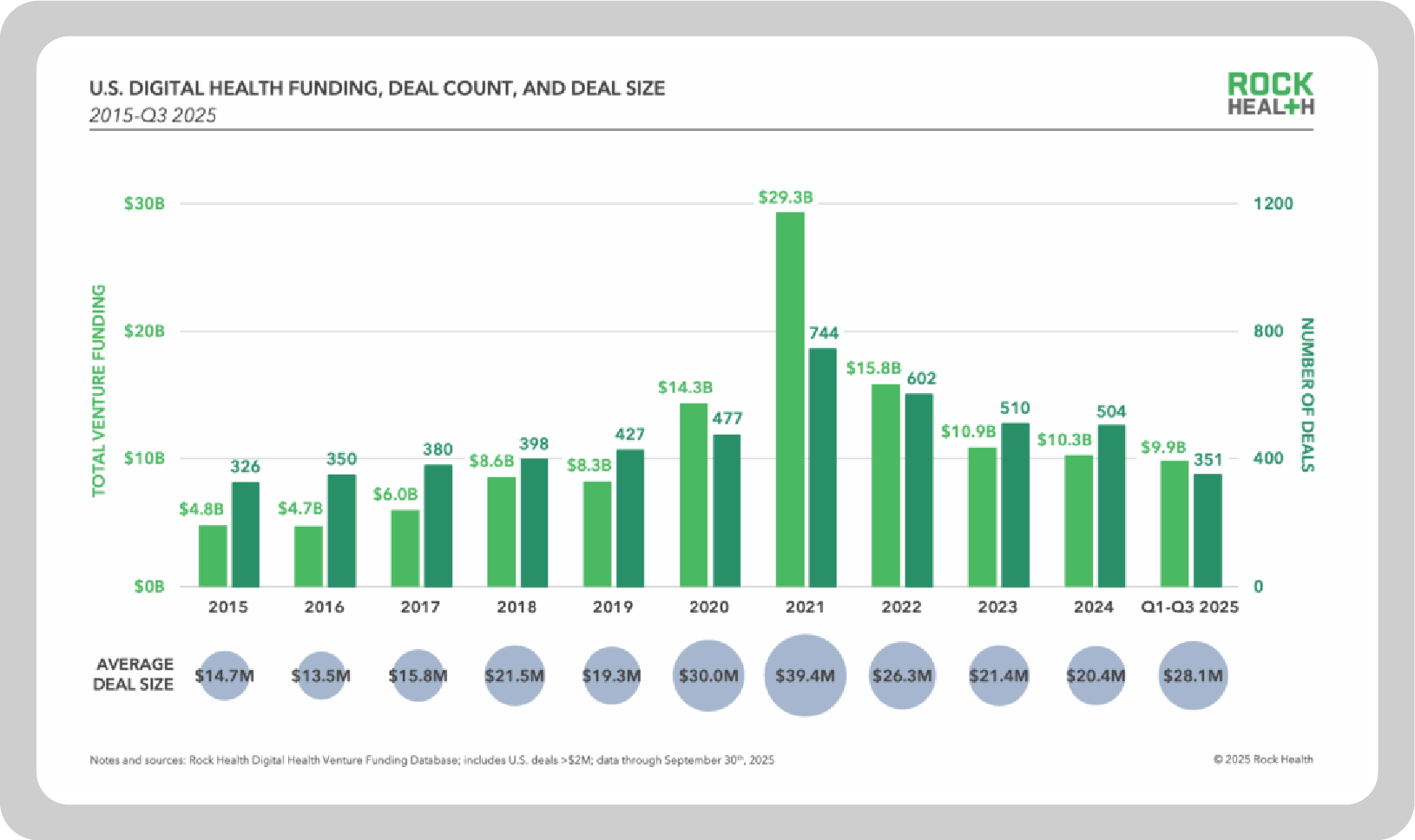

Rock Health — Q3 2025 market overview: Signals out of sync

Rock Health’s Q3 2025 report reveals a market that appears healthy ($9.9 B raised year-to-date) but masks a more turbulent reality underneath. Capital is concentrating in a shrinking pool of mega deals, while the traditional mid-stage ladder is eroding, forcing companies to prove maturity, differentiation, and ROI to survive.

Key Findings

- Funding concentration: $3.5 B raised in Q3 across 107 deals, with 19 mega rounds ($100 M+) representing 39% of all funding.

- Mega funds dominate: 80% of large rounds include Andreessen, Kleiner Perkins, or General Catalyst.

- Unlabeled rounds rise: 35% of financings are bridges/extensions, blurring traditional Series A/B signals.

- Series B bottleneck: Only 30 Series B deals so far in 2025 (half of prior years), but average check size $51.6 M.

- Workflow & infrastructure lead: 42% of funding flows to tools that optimize operations and integration; M&A up 37% YoY.

- Consolidation pressure: Startups are racing to go horizontal as incumbents absorb point solutions into core platforms.

Bottom Line: Digital health funding remains headline-strong but structurally uneven. The market is splitting between mega-funded winners and a thinning middle, rewarding those with clear ROI, scale, and defensible workflows — while leaving little room for narrative-only plays.

SVB — Future of Healthtech 2025: AI Supercharges Administrative Healthtech

Silicon Valley Bank’s latest Future of Healthtech report shows record 2025 investment — $18.5 B projected for the year — but with a major shift in focus: AI-enabled provider operations now dominate the sector, accounting for 44% of all funding and nearly three-quarters of mega-deals. The center of gravity has moved from clinical breakthroughs to workflow automation, billing, and documentation.

Key Findings

- Record investment: $18.5 B expected in 2025, the highest since 2022.

- Provider operations surge: 44% of all Healthtech investment; 73% of mega-deals.

- Capital concentration: 40% of the $1.5 B already invested went to a single company (Abridge).

- Valuations spike: Seed-stage AI valuations up 42% since 2021; mega-deal activity ↑ 38%.

- Alternative-care decline: Fell from 42% (2021) → 9% (2025); operations rose from 19% → ~50%.

- AI saturation: 52% of provider-ops deals involve AI, but SVB warns funding is outpacing adoption.

- Exit activity: 32 M&A deals YTD, with PE exits set to hit record highs; physician trust favors efficiency gains (75%) over privacy (15%).

Bottom Line: SVB highlights a healthtech market increasingly defined by back-office AI transformation rather than clinical disruption. The flood of capital and consolidation points to operational efficiency as healthcare’s next growth engine — but also raises questions about whether valuations can keep pace with real-world impact.

Inside HLTH 2025: Key Themes and Takeaways

Fresh from Las Vegas, HLTH 2025 delivered no shortage of big claims and bold ideas. As I was in the midst of moving across the country* right before the show, I was unfortunately unable to attend and reconnect with all my friends and colleagues this year, so I relied on others’ takes to keep up with all the news. Here are some of the headlines and hot takes that deserve a second look.

Newfire Friends Making Waves

It was great to see several of our partners making headlines at HLTH 2025. Humata Health took home the Rising Star in AI in Health Operations award and announced new partnerships with Microsoft and EviCore, underscoring how AI is transforming administrative workflows.

Knownwell, another company we’re proud to support, secured $25 million in funding led by CVS Health Ventures to scale its integrated obesity and metabolic care model. It’s rewarding to watch clients we’ve collaborated with continue to expand their impact and push the boundaries of digital health innovation.

A Private “Digital Safety Net”?

On the other side of the Medicaid equation, Cedar is stepping in to catch those who might fall through the cracks in the coming years during Medicaid redetermination cycles. The New York-based healthtech company, best known for billing tech, launched Cedar Cover, a “digital safety net” that helps patients keep Medicaid coverage and access financial aid. I find it striking that a payment platform is stepping into public-sector territory, connecting patients to benefits the government is likely to struggle to administer effectively and accurately during this next open enrollment period.

AMA Forays into Health AI Guidance

Finally, the American Medical Association launched its Center for Digital Health and AI to help physicians navigate the accelerating wave of technology in care delivery, focusing on:

- Policy and regulatory leadership: Working with regulators, policymakers, and technology leaders to shape benchmarks for safe and effective use of AI in medicine and digital health tools.

- Clinical Workflow Integration: Creating opportunities for doctors to shape AI and digital tools so they work within clinical workflows and enhance patient and clinician experience.

- Education & training: Equipping physicians and health systems with knowledge and tools to integrate AI efficiently and effectively into practice.

- Collaboration: Building partnerships across the tech, research, government, and health care sectors to drive innovation aligned with patient needs.

The AMA’s timing couldn’t really be much better given the recent spats between RFK Jr and CHAI (ABCO coverage), currently the de facto organization proposing how to regulate healthcare AI. This could portend a fracturing of these kinds of initiatives that makes it hard for developers of such solutions to know which recommendations to follow. As the administration has explicitly tried to stall any AI regulatory action following an “anti-woke” Executive Order back in July, it’s unclear what the future actually looks like for ensuring some standard set of rules around safety and ethics in an industry where that kind of guidance is critical.

My Recommended Takes from Attendees

HLTH always draws sharp opinions, but a few takes this year really cut through the noise.

Most Pragmatic Take: Abhinav Shashank

For a more grounded take than a lot of what you’ve likely seen circulating, Shashank argues that HLTH 2025 revealed a market entering a phase of AI fatigue, where leaders no longer buy technology for its own sake but demand proof of outcomes. Shashank also warns of a point-solution overload and a frothy funding climate reminiscent of 2021, suggesting the next phase of digital-health growth will favor consolidation, disciplined execution, and measurable value over hype, which is reflected in recent industry reports I covered earlier in this newsletter.

Most In-Depth Recap: Bryan Schnepf for HealthTech HotSpot

Bryan Schnepf offered the most in-depth take on HLTH 2025, capturing the conference’s full scope — from AI’s move into large-scale deployment to the mounting pressures of interoperability, cybersecurity, and workforce burnout. He framed the event as healthcare’s inflection point, where execution and integration — not invention — will determine which organizations turn innovation into measurable, system-wide change.

Most Public Health-Centric Analysis: Yimdriuska (Gigi) Magan

Gigi’s reflections from HLTH 2025 stood out for reconnecting the industry’s tech enthusiasm with its human purpose. Framed through themes like equity, Medicaid modernization, and empathy as measurable value, she reminded readers that innovation only matters if it strengthens care access and community health — the spaces where technology meets humanity.

Most Forward-Looking Perspective: Steven Farmer for ABIG Health

Steven Farmer provided an expansive view of HLTH 2025, tracing how AI integration, regulatory uncertainty, and renewed physician influence are reshaping healthcare’s next chapter. His takeaway was both optimistic and grounded: the future of innovation will hinge on governance, inclusivity, and trust — AI that enhances care, investment that reflects patient diversity, and collaboration that bridges policy, technology, and human purpose.

Money Moves: October’s Notable Funding and M&A Deals

This month’s funding and acquisition news suggests that confidence is quietly returning to healthtech and that the IPO window may be cracking open again.

Claude’s move into life sciences caught my attention. Anthropic launched Claude for Life Sciences with integrations across Benchling, BioRender, PubMed, and Wiley — essentially giving researchers conversational access to their data and literature. It’s a logical next step for foundation models, and it lands just as OpenEvidence raised another $200 million to build its “ChatGPT for medicine.” Together, they signal a serious push to make AI usable in workflows extending into other areas of medicine, not just clinical documentation.

Oura’s $900 million round led by Fidelity looks, to me, like a pre-IPO raise — the kind that funds infrastructure and regulatory readiness rather than product expansion. If they pull it off, it could mark one of the first major consumer healthtech IPOs since 2021.

On the M&A front, Qualtrics acquired Press Ganey for $6.75 billion, merging experience analytics with healthcare data, while Premier Inc. agreed to go private in a $2.6 billion deal. Taken together, these moves point to a market consolidating around scale, data ownership, and the operational layer of healthcare innovation.

Around the Web

Cohere Health and Microsoft Partner on Ambient Prior Authorization

This confirms the direction ambient scribe companies are taking: moving beyond documentation into full administrative automation. Microsoft’s pairing its Nuance ambient tech with Coher Health’s utilization management system to streamline prior auth, and I expect we’ll see a lot more of these deals as others scramble to catch up.

ACA Premiums Set to Spike 30% Without Federal Subsidies

This one’s alarming. Without subsidies, average ACA premiums could jump as much as 30%, and in some markets even double, a direct consequence of the ongoing budget stalemate. That’s going to push more Americans into catastrophic plans, delay care, and take an estimated $32 billion out of hospital revenue next year. Expect innovation budgets to tighten sharply if this holds.

Epic Winds Down Its Startup Codevelopment Program

Epic ending its Workshop program looks like a cover-your-bases move after the bad optics with Abridge and its own competing scribe launch. It’s not a huge surprise — they’ve been flirting with antitrust risk for a while — but it does show how incumbents are closing ranks and limiting potential vectors of exposure as more anticompetitive scrutiny is applied to the EHR space.

Shutdown Fallout Deepens Across Healthcare

As the federal shutdown drags into its third week, we’re seeing the first signs of real disruption — delayed reimbursements, paused grants, and budget freezes. The timing couldn’t be worse: if this persists, health systems will go into 2026 on financial defense, pulling back from software rollouts and new tech adoption, sending even more shockwaves across the innovation sector.

That’s My Take. What’s Yours?

Healthcare is evolving fast, and while some trends make headlines, others quietly redefine how care is financed, delivered, and scaled. I’ll be back next month with more signals (and hopefully a few answers) to where the market is headed next.

Don’t want to wait? If you’d like to talk through how these dynamics connect to your current strategy or portfolio, let’s start that conversation today.